There are many misconceptions about your credit score needed to buy a new home. It was reported that one-fourth of renters believe they need a credit score of 780 – 800 to be considered for a mortgage. They are misinformed.

Only 25% of Americans have a FICO® credit score between 740 and 800. According to Experian, 16% of Americans have a credit score between 300 and 579. This is considered very poor credit. 18% have a fair credit score between 580 and 669. 21% have a FICO® score between 670 and 739. This is considered good credit. Only 25% of Americans have a very good credit score between 740 and 799. And only 20% have an exceptional rating between 800 to 850.

There are three major credit reporting companies: Equifax, Experian, and TransUnion. Obtaining your credit report is as easy as calling and requesting one. Once you receive the report, it’s important to verify its accuracy. Double-check the high credit limit, total loan, and past-due columns. It’s a good idea to get copies from all three companies to assure there are no mistakes since any of the three could be providing a report to your lender. Fees range from $5 to $20 and are usually charged to issue credit reports but some states permit citizens to acquire a free report. The federal government provides a free report at

annualcreditreport.com.

FHA and VA Loans

The Federal Housing Administration (FHA) now requires a minimum FICO® score of 580 if you want to qualify for a home loan. FHA loans require lower (minimum) down payments and credit scores than many conventional loans. Your down payment can be as low as 3.5% of the purchase price. Most lenders require a score of at least 640.

Veterans Affairs (VA) loans have no credit score requirements. There are different types of VA loans. With a VA direct home loan, the government is your mortgage lender. That means you will work directly with them to apply for your loan. With a VA-backed loan, the government guarantees a portion of the loan you get from a private lender. Nearly 90% of all VA-backed home loans are made without a down payment.

Randy Hopper, Senior Vice President of Mortgage Lending for Navy Federal Credit Union said, “Just because you have a low credit score doesn’t mean you can’t purchase a home. There are a lot of options out there for consumers with low FICO® scores.” There are many programs available with low or no credit score requirements.

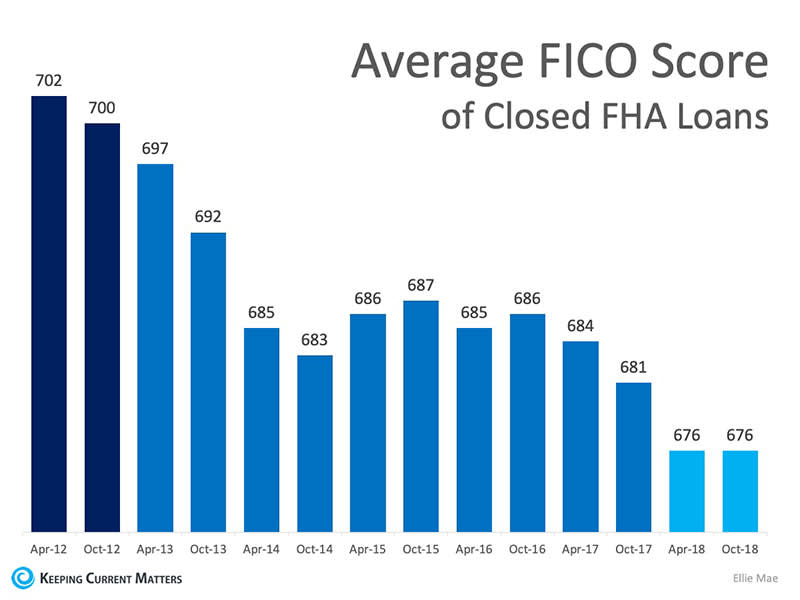

As you can see from the agencies above, none of them require a credit score above 700! There are plenty of people taking advantage of the low credit score requirements. Below is the average FICO® score of closed FHA loans.

As you can see above, the FICO® score numbers have been dropping for the last seven years. As a matter of fact, the average FHA loan FICO® score reported earlier this year was only 675. The average American is unsure about their credit score. They just assume that it is too low to qualify for a home loan and don’t double-check.

Credit.com stated that only 57% of individuals checked their credit rating at least once last year.

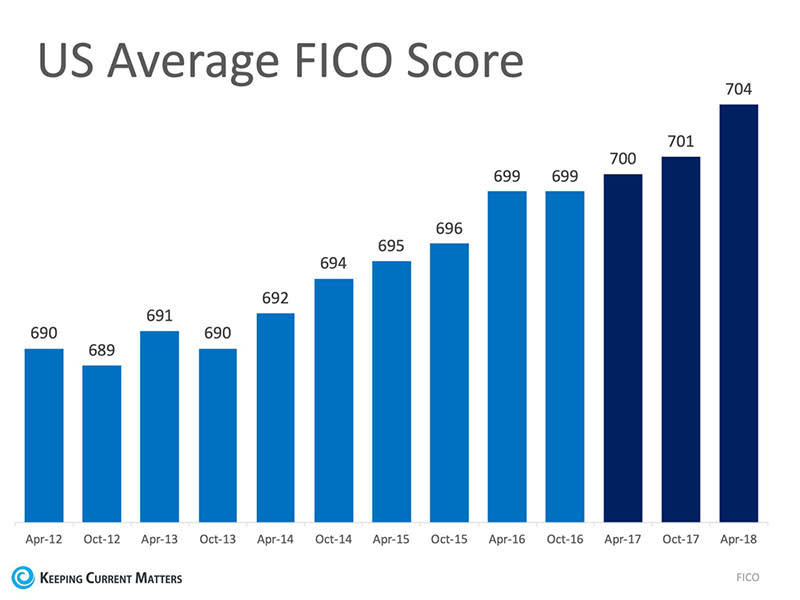

FICO® reported, “Since October 2009, the average year-over-year FICO® score has steadily and consistently increased, from a low of 686 in 2009 to the latest high of 704 as of 2018.”

Below is the increase in the average US FICO® score over the same period of time as the graph earlier.

Your Credit Score and a Home Loan

So, what does this mean for you? At least 84% of Americans have a credit score that would allow them to buy a new home. If you are unsure what your score is or would like to improve your score in order to become a homeowner, contact a

Real Estate Broker at Wenzel Select Properties in Downers Grove. Call

(630) 430-4790. We can help you to set a path to reach your dream and buy a new home.