Buying vs Renting

Buying a home to build equity is one of the main financial reasons for prospective home buyers. Another is about freedom. You can paint the walls whatever color you want, add a deck or patio, and park in your own garage. Here are a few buying vs. renting points to consider when deciding whether buying vs renting makes better sense for you.

Reasons for Renting

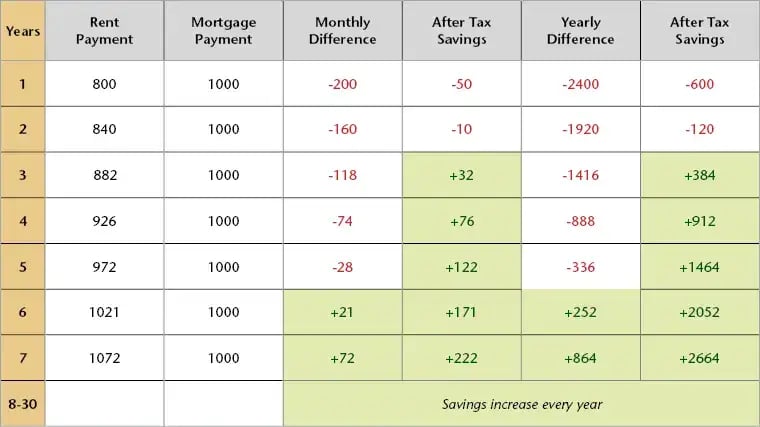

Renting is simple and you don’t have to worry about being tied down to a place for too long or having to stress about maintenance or homeowner’s association fees! Here are a few reasons why you may want to rent vs buying a home. What you may not realize, is that you are essentially paying for someone else to own the property you rent and throwing your own money away when you can invest it for yourself. In the below chart, you will see the comparison of a renter vs. a homeowner over a seven-year period.

- Flexibility – Renting allows you to get familiar with an area before making the longer-term commitment of buying a home.

- Maintenance – When a toilet breaks, you call the landlord.

- Job – If you think you might need to move in the near future, you may want to rent.

- Income – If you expect a pay hike or cut, that can impact your ability to pay a mortgage.

- Utilities – In some cases, utilities such as water, garbage, and heat are included.

- Bad credit – Creating a history of on-time rental payments can help build the credit you’ll need to qualify for a mortgage.